Budget Modification

If your program encounters unexpected decreased or increased expenses in various line items, a budget modification may be necessary. Budget modifications occur when there is a:

- Shift of funds from one budget category to another

- Shift of funds from one section to another

- Reduction of the grantee share (match)

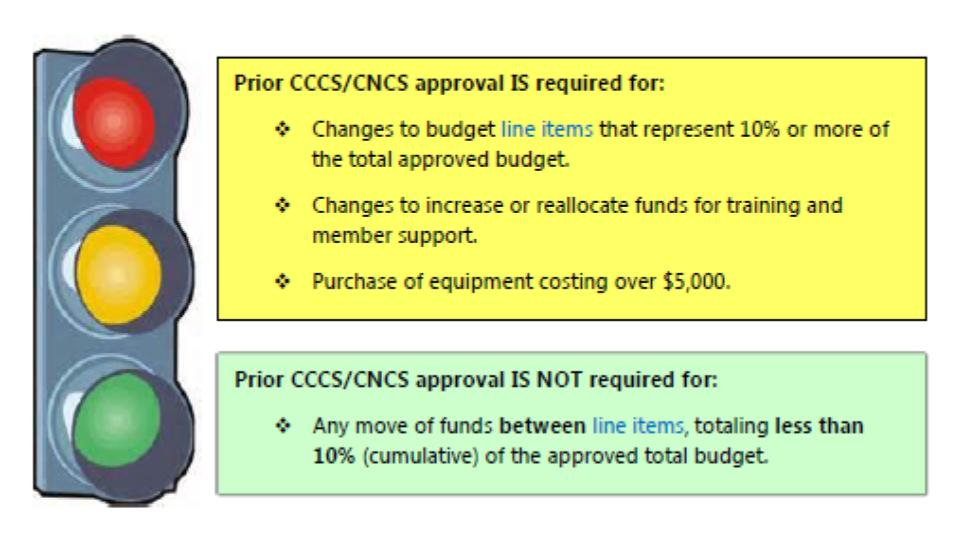

The Corporation acknowledges that budget revisions are sometimes unavoidable and sometimes are required more than once in a program year. Thus, programs may move funds between line items without Commission or CNCS approval if the cumulative amount moved is less than 10% of the total grant amount, as long as the transfer is in compliance with all applicable standards and requirements articulated in the grant agreement and/or AmeriCorps Regulations (45 CFR§2543.25).

Example: A program that receives a $100,000 grant may move a cumulative total of up to $9,999.99 between line items without Commission or CNCS approval as long as the transfer is in compliance with all other applicable standards and requirements.

Programs that wish to transfer funds totaling 10% or more of the total grant award, wish to increase or reallocate funds for training and member support, or to purchase equipment costing over $5,000 must submit a budget modification request via the Commission's OnCorps Reporting Portal and receive prior approval from the CCCS and CNCS. Programs should explain changes made to the revised budget in the space provided for justification of changes on the request form. Programs should not consider budget modification requests approved until written notice of approval is received from the Connecticut Commission via the OnCorps Reporting Portal and/or the Corporation. Questions about budget modifications should be directed to the CCCS Executive Director. Instructions for submitting a Budget Modification Request in OnCorps are accessible in the OnCorps Reporting Portal Help platform.